RELATED NEWS

- Spanish Furniture Trade Report: 2025 and Q1 2026 Analysis

- Feria Hábitat València 2026: Where Mediterranean Soul Meets Global Design

- Feria Habitat Valencia 2023: The International Showcase for Spain’s Interiors Industry

- Salone del Mobile.Milano 2023. The Spanish furniture industry will be back in force to the Salone with a collective participation of 37 brands

- Feria Habitat Valencia 2022. The most important event of the Spain furniture industry is back again in September

- Spanish furniture trade: 2021 annual report

- Spanish furniture trade: 2019 annual report

- Furniture from Spain starts its trade show circuit at the IMM COLOGNE 2018

TAGS

- spanish furniture industry

- spanish furniture trade

Spanish Furniture Trade Report: 2025 and Q1 2026 Analysis

The Spanish National Association of Furniture Manufacturers and Exporters (ANIEME) has released the Spanish furniture foreign trade report for the year 2025 and the first trimester of 2026. Figures reveal that, during the 2025 period, Spain’s furniture exports grew by an impressive 5.0%, exceeding 3,146 million euros. It is worth highlighting the sector’s market diversity and its highly positive performance in countries like France, Germany, Italy, and Poland, which has successfully shielded Spanish manufacturers against a highly volatile global climate.

1. Global Furniture Market Outlook

The global furniture market, valued at over USD 440 billion, operates within a highly complex macroeconomic environment where industrial performance is actively shaped by shifting consumption patterns and persistent geopolitical tensions. While 2025 was marked by policy uncertainty, protectionist measures, and rising tariffs, it still managed to deliver positive export results for resilient markets before broader consumption began to stagnate. Moving into 2026, the global market faces another major test of resilience. Since February 2026, international attention has shifted heavily to the Middle East, where the volatile geopolitical situation is exerting a significant impact on the Gulf countries, directly slowing down regional tourism and stalling the numerous large-scale construction projects currently underway.

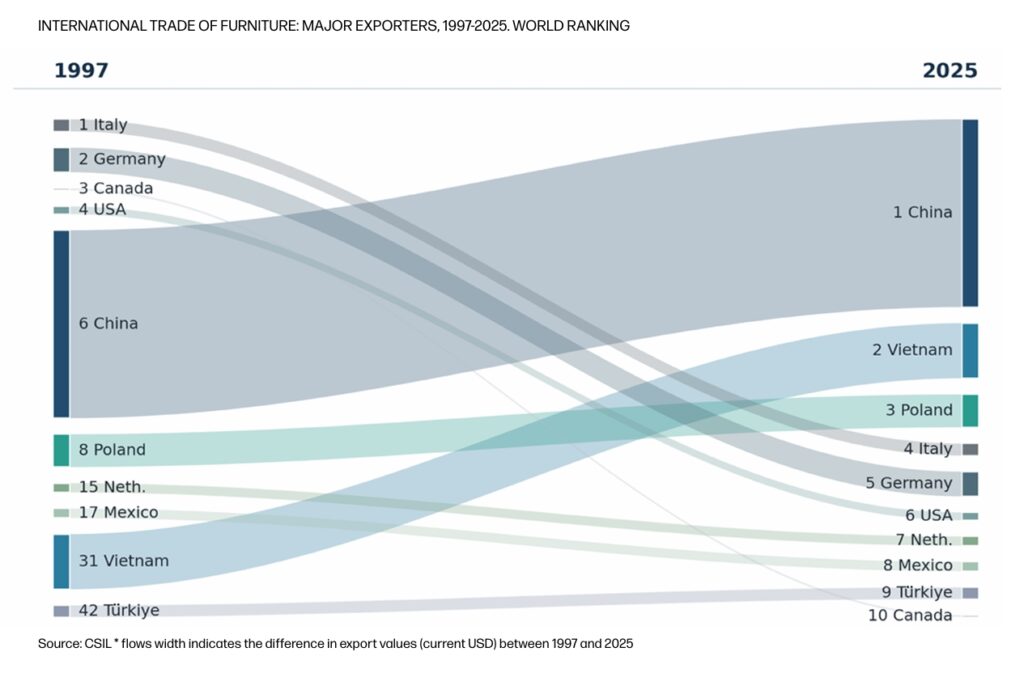

2. International Trade and Tariffs: Realigning the Global Map

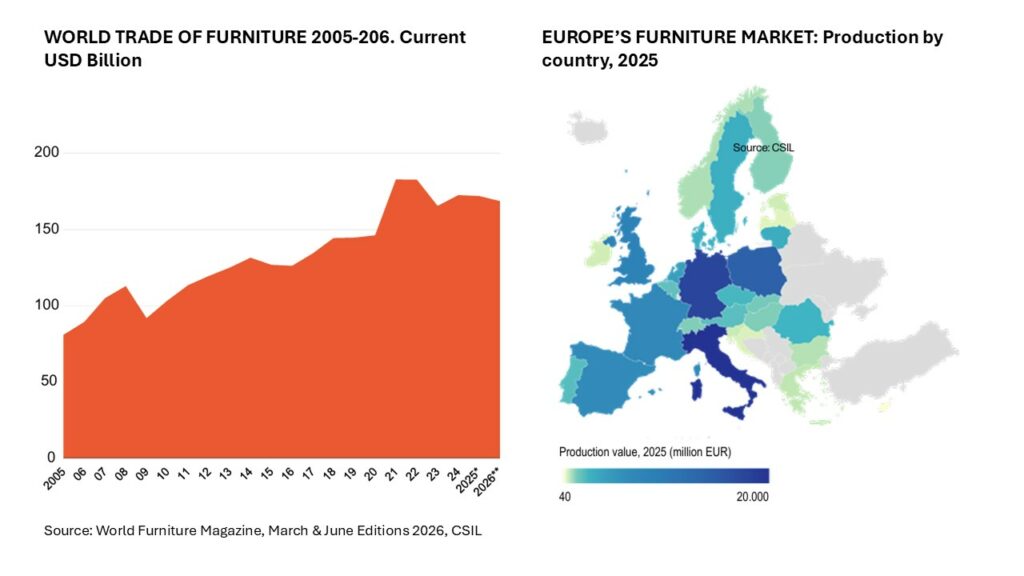

The traditional mechanics of international furniture trade have entered a less predictable phase, shifting away from decades of centralised manufacturing toward regionalised, protective strategies. A striking divergence emerged in 2025 as global manufacturing trade accelerated while international furniture trade remained flat at approximately USD 170 billion, pointing to a selective rebalancing of trade routes influenced by tariff uncertainty, logistics costs, inventory strategies, and the search for more reliable supply chains. This structural shift is clearly reflected in regional corridors where intra-European trade expanded, while the Asia-to-North America corridor, by contrast, contracted by ten per cent—a direct consequence of US tariff escalation and the resulting supply chain adjustments.

3. Europe’s Market Malaise and Spain’s 2025 Resilient Success

The intensity of the European furniture market differs sharply by local conditions, revealing a clear divide between struggling core economies and Spain’s standout performance. Throughout 2025, France and Germany continued to register the weakest results in Europe, severely constrained by very soft domestic demand and low consumer confidence. Italy posted a modest contraction, driven primarily by declining foreign sales, while its domestic demand slipped slightly. Spain, by contrast, recorded a highly positive performance in 2025, a year in which Spanish exports registered a significant +5%, supported by firmer household spending and a much more dynamic domestic housing market.

According to official ANIEME and ICEX data, Spain closed the 2025 exercise with total furniture exports reaching 3,146.5 million euros, marking a robust 5.0% growth compared to 2024. This exporting strength left Spain with an annual trade coverage rate of 76.4%. In terms of destination markets for 2025, France maintained its undisputed leadership with 817.9 million euros (a 26.0% share), Portugal held second place at 15.7%, and the United States ranked as the top non-EU destination in third place with a 5.8% share, while Poland emerged as the most dynamic top-ten market of the year with an impressive export growth of 23.7%. On the import side, Spain brought in 4,120.5 million euros of furniture in 2025, an 8.0% increase, with China remaining the leading supplier, holding a 30.3% share of the import market. Read the full report>>>

4. First Trimester 2026: Spanish Foreign Trade Performance

Data from the first trimester of 2026 reveals a cyclical correction in Spanish furniture trade, echoing the global climate and the cooling of key neighbouring economies. Total Spanish exports for the quarter reached 691 million euros, representing an 8.0% decrease, while imports fell by 8.2% to 991 million euros, allowing the national trade coverage rate to remain stable at 69.7%.

France confirmed its status as Spain’s primary export destination by absorbing 212 million euros during the quarter, despite a moderate 5.1% decline caused by its cooling retail market. Reversing their sluggish 2025 domestic trends, Germany and Italy positioned themselves in third and fourth place by recording positive import growth from Spain during these opening months, proving that Spanish contract and design solutions remain highly competitive in mature European hubs. While exports to the United States suffered a sharp contraction of 24.0% due to the ongoing transatlantic tariff realignments, Poland sustained its exceptional momentum from the previous year, emerging as a dynamic standout in ninth position with an export growth rate of 48.7% and demonstrating the successful regional diversification of Spanish manufacturers.

In conclusion, while the cyclical correction in the first trimester of 2026 reflects a tightening global economy and geopolitical disruptions in key regions like the Middle East, the structural foundation of Spain’s furniture trade remains resilient. By leveraging high design adaptability and expanding deep regional corridors within Europe, Spanish exporters are successfully mitigating broader macroeconomic pressures. Maintaining this strategic diversification will be essential for navigating the selective rebalancing of global supply lines moving forward.

Source: CSIL (WFM March & June 2026), ANIEME, ICEX